Have we been lying by calling the eviction moratorium a moratorium?

Eviction armageddon seemingly imminent as millions remain behind on rent, billions of aid lies unspent, and the moratorium expiration days away

Short on time? Read to the red line for the highlights. Want to learn more? Items that are bolded in the top section are expanded upon beneath the red line.

During the pandemic, this once-per-month newsletter may be split into two issues: one monitoring developments related to the COVID-19 pandemic, and one for other news on housing justice.

Links to our projects: Housing for All podcast | Housing for Us podcast | YouTube channel | previous issues of this newsletter | recommended reading | homepage

Arthur Tarley argues that it’s simply a lie to call the federal eviction moratorium a “moratorium” or a “ban”:

Another distortion: calling a policy an eviction “moratorium” or “ban” when people are still being evicted and are still under threat of eviction. It’s another example of how many of America’s top Democrats, with the help of the mainstream media, are intentionally misleading the public, as evidenced by headlines like “Biden extends the national ban on evictions through March 2021” and “Biden administration extends federal eviction moratorium through end of June.”

...With that in mind, how is the public supposed to make sense of headlines like, “Millions of Americans could lose their homes despite President Biden’s eviction moratorium order,” “Colorado’s Eviction Moratorium Is About To Get Looser,” and “The CDC banned evictions. Tens of thousands have still occurred?” CNBC reported that between the September CDC “eviction moratorium” and early December, there were tens of thousands of evictions. Definitionally, there’s a problem here[:] the policy is not actually a moratorium, our leaders know it’s not a moratorium, the media knows it’s not a moratorium [—] but everyone still calls it a moratorium and our leaders frame it as a moratorium to the public.

He argues that calling a grossly incomplete policy a “ban” or “moratorium” is simply propaganda, that it intentionally misleads people about reality for a political purpose:

Focusing so heavily on the so-called moratorium not only rhetorically concealed the evictions taking place across the country, it also obscured the future reality that unless eviction protections are made permanent (or back rent is forgiven), many more people will be facing eviction in due time.

In other words, people who know how incomplete the policies are, are demanding policies actually congruent to the scope of the problem. It’s easier for elected officials if too many people don’t know how bad the situation is; [otherwise, they’d be forced to actually do something].

Photo: “Evicted” by Joris Louwes

Not so relaxed anymore

Last issue, we noted how relaxed housing experts were about the slow pace of rental assistance getting to renters behind on rent. One of the US’s leading voices for affordable housing was quoted on April 25: “I think it’s going to be OK.”

Fast-forward a month. Here’s an article published on May 24th; with the federal eviction moratorium expiring on June 30, housing experts are apparently way less relaxed:

But with the federal eviction moratorium expiring at the end of June, and several judges attempting to strike it down before then, states may have mere weeks to get money into the hands of renters before eviction processes start up again in earnest.

Not a single expert or advocate Vox spoke with believes the money will be allocated by then.

Hardly any money has actually been spent (emphasis added):

Tenant advocates I spoke with in California and Washington, DC, told me they didn’t personally know anyone who had actually received aid.

Georgia’s Department of Community Affairs told me that it has distributed more than $4 million in rental assistance funding to landlords and tenants; the state has received over $552 million for that purpose. Delaware’s State Housing Authority told me that it has distributed $40,000 in rental assistance — 0.02 percent of its allocated funds. The Idaho Housing and Finance Association told me it has distributed $6.1 million of the $175 million it received from the December congressional rent relief allocation. Colorado’s dashboard shows $2.8 million has been approved from the $247 million it has received. Arizona’s dashboard shows $4.38 million has been disbursed out of the $289 million it has received.

More has reached tenants — those state numbers don’t include the spending done by programs at the county and city level — but it indicates the pace of these programs may not be fast enough to meet the urgent, coming crisis.

The New York Times recently reported that California had only paid out $1 million of the $355 million requested by tenants and landlords. The Times also reported that Texas, which has received over $1 billion, had only paid 250 households after 45 days. Some states are not even accepting applications for emergency rental assistance, including New York.

As we discussed last issue, there is no way to track where the $59.8 billion in emergency rental assistance is going, so it’s impossible to know just how bad things are. But all data point to disaster. As of June 14, the National Low Income Housing Coalition reports that they have been able to use public data to figure out how much emergency rental assistance money has been distributed in 13 states. “Combined, these 13 states have approved or distributed approximately 11% of their first-round ERA allocations. The amount of overall allocation approved and distributed in each state varies widely, however, from .1% in Wyoming to 25.8% in Texas.”

But remember, “approved” does not mean the money has actually gotten to needy renters. California was allotted $355 million, yet has only approved $20 million to be paid out to cover unpaid rent. But of that $20 million, only $1 million has actually been paid out. South Carolina hasn’t been able to pay out a single dollar. Some local programs also haven’t been able to spend a single dollar.

Why are things going so badly? In a previous issue, we looked at many reasons why previous rounds of aid went unspent, and we’ll see below how these issues still have not been solved. First, the application is extraordinarily difficult to complete; completed applications are hundreds of pages long and measure an inch thick. Very few people are able to collect the information and supporting documentation needed to apply. Many eligible renters are unaware of the program. And perhaps most vexingly, many landlords are simply refusing to accept emergency rental assistance, choosing to throw their tenants to the street rather than accept thousands of dollars in cash. One study found that a third of landlords refusing to participate were actually facing bankruptcy. You did not misread that: a large number of landlords are facing bankruptcy yet still would rather evict tenants than accept thousands of dollars in cash from emergency rental assistance programs.

The situation is getting worse, not better

With the federal eviction moratorium set to expire on June 30, how many renters are behind on rent and how much do they owe?

National Equity Atlas’s most recent estimates (covering May; their estimate for the number of renters households behind on rent is Household Pulse’s data) hold that 5.8 million renter households are collectively behind on $20.3 billion in rent, or approximately $3,500 per household. Last month (covering April), they estimated 5.7 million renter households were behind on rent, totalling $19.8 billion, or $3,400 per household. The number of households behind on rent, the aggregate total amount they are behind, and the amount owed per household all increased.

And, according to the most recent Household Pulse, 14% renters are not caught up on housing payments; that amounts to 6 million households. The number of renters behind on rent is increasing, from 5.7 million in April, 5.8 million in May, and 6 million in June. The problem is getting worse, not better. Remember that these are households, not individuals. Since most households contain more than one person, 6 million households is far more than 6 million people (it’s likely well over 10 million people).

Another way to estimate the scope of the problem is to see what beneficiaries have been awarded. For the 13 states the National Low Income Housing Coalition is able to track:

“On average, programs are paying out $4,723 per household, though this ranges by state from $2,630 in Nebraska to $6,580 in Connecticut. These differences are expected, given the varied costs of living and amount of months covered across states.”

In sum, all available data point to millions of households owing thousands of dollars in rent — sums unpayable without emergency cash assistance. Unable to access emergency rental assistance, the expiration of the federal eviction moratorium will be a catastrophe of historic proportions.

Some state and local moratoria will protect tenants beyond June 30; Eviction Lab has a run-down of state protections (or lack thereof) and when they expire.

The Biden Administration may yet extend the federal eviction moratorium; it has been extended twice since December, with President Trump waiting until just four days before its expiration on December 31, and President Biden waiting until just two days before its expiration on March 31. We wrote of Trump’s December extension:

“If you’re not one of them, try to imagine the terror tens of millions of Americans who can’t afford rent must have felt not knowing if they would have a place to live until 4 days prior to doomsday.”

But legal challenges to the federal eviction moratorium are getting more serious, which we also reported on last issue. And, the federal eviction moratorium is a measure of the Centers for Disease Control and Prevention (CDC), which has the power to enact emergency measures to prevent the spread of infectious disease. But as more and more people get vaccinated, the eviction moratorium is becoming unnecessary to prevent the spread of the coronavirus; in other words, the statutory authority for the CDC to enact the moratorium is rapidly evaporating. Even if the Biden Administration decides last minute to extend the moratorium, it may not survive much longer.

Meanwhile, renting is getting even harder

As if things weren’t bad enough already, rents are surging nationwide. From Apartment List:

Our national index increased by 2.3 percent from April to May, representing the third straight month of record-setting rent growth, going back to the start of our rent estimates in 2017. After this recent spike, year-over-year rent growth now stands at 5.4 percent nationally…

[T]he data continue to exhibit significant regional variation, and there are still a number of markets where rents remain well below pre-pandemic levels. But even in these markets, the trend has turned a corner. Rents in San Francisco, for example, are still 17 percent lower than they were in March 2020, but the city has seen prices increase by 13 percent over just the past four months. 9 of the 10 cities with the sharpest year-over-year declines have now had four consecutive months of rising rents. At the other end of the spectrum, many of the mid-sized markets that have seen rents grow rapidly through the pandemic are showing that there’s still steam left in the current boom — Boise rents jumped by a staggering 6.6 percent just this month and are up 31 percent since the start of the pandemic.

And, via CNBC:

Just as home prices are rising due to low supply, rents are jumping as well. Rental rates increased 1.3 percent year-over-year in April, which doesn’t sound like a lot but it’s the fastest acceleration in a decade. For single-family homes, where the renters likely include a lot of disappointed buyers locked out of the home market, that increase went up to 4.3 percent year-over-year. And for single-family rentals owned in bulk by Wall Street landlords, that acceleration has nearly doubled, to around 7 percent year-over-year.

Overall, far better news on the homeownership side

Rents are not the only housing prices soaring: prices for owner-occupied homes are also skyrocketing. Black Knight’s most recent report states:

We’ve now seen 17 consecutive months of home price increases, with the growth rate accelerating sharply in recent months[, and] April saw the highest annual home price growth rate on record (14.8%) since Black Knight began tracking the metric in the mid-1990’s[.] Single family homes led the way, with prices up 15.6% from the same time last year, also an all-time high, while condo prices are up 10% year-over-year.

Idaho leads US states with a shocking 33% year-over-year increase in home prices, and Austin leads US metropolitan areas with a 25% year-over-year increase.

The report cites more data showing the unprecedented scale of home price increases, and it’s impossible not to get flashbacks to the disastrous housing crash of 2008-9. However, David Dayen argues that despite surging prices for homes for homeownership, this phenomenon is not a new housing bubble.

While an eviction armageddon appears inevitable, the news is much brighter on the homeownership side. We continue to be on track to avoid a foreclosure armageddon, in part because pandemic protections for homeowners were far better — and scheduled to remain in effect for far longer — than protections for renters.

Miscellaneous

In past issues, we looked at the (limited) evidence that renters were already buckling under rent costs, and the pandemic didn’t actually affect tenants’ ability to pay rent very much. Another dataset argues that the pandemic really did stop a lot of people from paying rent. Another survey of landlords in Philadelphia done by the Housing Initiative at Penn found that, “Since the pandemic began, the share of owners experiencing issues with tenant nonpayment has doubled from 25.9% to 51.5%.”

A new law in Oregon gives tenants until February 28, 2022 to catch up on rent; it also keeps evictions caused by the pandemic off credit reports and court records, protecting unlucky tenants from the many negative long-term impacts of having an eviction. A new law in Illinois also seals all records of evictions during the pandemic.

It’s no surprise that the Mortgage Bankers Association and their allies want the federal eviction moratorium to come to an end. But this press release deserves an award for being out of touch, disingenuous, or both in claiming, “The continuation of a nationwide one-size-fits-all, federal eviction policy is at odds with the current economic environment and will ultimately only serve to place insurmountable levels of debt on renter households and impede the recovery in the housing sector.” (emphasis added). So ending the eviction moratorium will actually help the growing numbers of people behind on rent. Right.

We haven’t come across many stories about authorities trying to enforce eviction moratoria, but here’s one: the Minnesota attorney general sued a landlord who forced a family out in spite of the state’s ban on evictions. The landlord wanted the tenants out so she could sell the property. The landlord had to pay the family $3,573.86. That’s a slap on the wrist, especially considering the landlord likely made a great deal of money selling real estate in a very hot market. Minnesota is currently suing another landlord. A+ for effort, but enforcing something so important shouldn’t require a state attorney general to sue individual landlords, one by one.

Add Idaho to the list of places where evictions have returned to pre-pandemic levels.

A St. Louis landlord was caught taping a forged eviction notice on a tenant’s door in an attempt to circumvent the eviction moratorium.

The disaster of Emergency Rental Assistance programs

Only a small amount of the $59.8 billion the Biden and Trump administrations have allocated for emergency rental assistance has actually gotten to people in need. Why has this been such a fiasco?

Applying for emergency rental assistance is like deciphering Cretan hieroglyphs

The Washington Post did a deep dive on one agency’s struggles in Decatur, IL. The piece really is worth reading in full:

Shane Hartman figured that giving away badly needed rental assistance in a city battered by the pandemic recession would be relatively easy. But five months after his nonprofit was tapped by city officials to hand out more than a half-million dollars in federal aid, he had distributed only $44,772, and had helped just 21 families.

The problem wasn’t a lack of need. Decatur’s unemployment rate hovered around 10 percent, compared with about 6 percent nationally. Hartman heard regularly from people who were months behind on their rent and desperate for help. But too many of those who came to his office seeking aid gave up before completing the eight-page application that required dozens, and in a few cases hundreds, of pages of financial documents.

By early May, a pile of more than 50 half-finished application packets sat on his desk.

“I would love to have a conversation with someone who wrote these rules and ask them: ‘Do you realize how hard you’ve made it to spend this money?’ ” Hartman said. “ ‘Do you get it? They can’t. There’s no way.’ ”[...]

The upshot for Hartman: He still had $467,038 in rental assistance that was proving almost impossible to spend. He plucked an unfinished rental assistance application from his growing pile and dialed the cellphone number on the form. He was trying to reach 49-year-old Toni Snipes, who owed more than $4,000 in back rent and electric bills.

“Is this a bad moment?” asked Hartman, who could hear a rustling in the background.

For now, Snipes was just another harried, stressed-out voice on the phone; someone desperately in need of the aid that Hartman could not seem to share. He ran through the documents missing from her application: her past six months of pay stubs, her tax returns and something he could use to prove her loss of income was caused by the coronavirus pandemic.

Then he noticed a problem.

The easiest way to prove a loss of income due to the pandemic is a letter from an employer confirming that the person seeking aid had been laid off. Snipes’s last job was for a temp agency, and Hartman knew from experience that they almost never signed such letters. He hung up the phone and dropped Snipes’s application back on the pile.

Basically the worst scavenger hunt of all time.

He realized he had a problem in January when his first successful aid applicants — a married couple that had been laid off from the city’s Caterpillar truck plant — had finished their application. It was more than an inch thick...Some of his clients struggled with literacy and had trouble with questions such as one that asked them in a few sentences to “explain or describe [their] change in income.” Others were put off by requirements that they produce six months of pay stubs, a copy of their lease and the previous year’s tax returns.

Emergency rental assistance programs can’t cut through all the red tape, either

The program isn’t just onerously burdensome for tenants in need; it’s difficult for the programs themselves. For a dramatic example, New York City — home to a huge portion of American renters — couldn’t get their online application up and running until June 1 — just 29 days prior to the end of the moratorium.

Some still don’t even know the program exists; many have barely been given an opportunity to apply

Vox has a story of a woman so desperate for money she accepted money to have fertility doctors harvest eggs from her uterus:

“I’m terrified. I’m so terrified to spend money,” the 31-year-old Floridian told me as she shopped at Walmart for household supplies. “I literally donated eggs to [make rent]. I’m selling off body parts.”

Ashbes, who says she works 11- or 12-hour shifts without a break at a Texas Roadhouse to afford her $1,300-a-month rent, didn’t even know she could apply for rent relief.

Technically, she couldn’t, until the week before last when the state opened up its rent relief application process, the Tampa Bay Times reports. Meanwhile, Miami-Dade County, where Ashbes resides, has already closed its program for applications.

Take the @#$% money!

As we’ve previously reported, many landlords are simply refusing to accept emergency rental assistance, turning down thousands of dollars to instead put their tenants out on the streets. Examples abound. In Houston, 8,000 desperate renters could not receive emergency rental assistance because their landlord hadn’t registered with the local emergency rental assistance program. In LA, a shocking half (49%) of landlords surveyed (h/t) did not participate in a 2020 emergency rental assistance program. This cruelty is difficult to understand; the researchers ultimately couldn't explain the lack of participation, writing:

Surprisingly, over one third of owners who did not participate in the 2020 ERAS [LA’s emergency rental assistance] program said their rental businesses could survive for less than 3 months in the current environment. This raises the question of why owners who were so adversely impacted by the pandemic did not participate in a program that offered rental subsidy.

After a landlord group urged the Supreme Court to overturn the federal eviction moratorium,

Diane Yentel, president of the National Low Income Housing Coalition, said the landlords' appeal to the nation's highest court was "astonishing" because $50 billion in funding was available nationally to pay the rent arrears owed to them.

"If they spent even a quarter of that effort instead convincing landlords to apply for and accept the money," said Yentel, "maybe they wouldn’t feel such a pressing need to evict low-income tenants who fell behind on rent during the global pandemic."

It’s cynical for another reason: many landlords do not actually have to pay their monthly mortgage payments. Fannie Mae and Freddie Mac offer forbearance plans for landlords unable to pay their mortgage due to the pandemic (they recently extended this program to September 30, the third such extension). As we discussed in the final episode of Housing for All, about half of all mortgages for 5 or more unit apartments are owned by Fannie or Freddie.

All data point to failure

Overall, as we lamented last issue, it’s impossible to actually know very much about how much rental assistance has actually gotten to those who need it — there is no way to monitor the hundreds of local agencies that have been entrusted to actually distribute that money to needy renters. We simply don’t know for sure how bad things are, but every piece of evidence argues that the expiration of the eviction moratorium will be a very dark day.

Prices for owner-occupied homes surge

David Dayen on furiously rising home prices:

The current national level of home prices, adjusted for inflation, sat in March at 4 percent above the peak of the housing bubble that led to the Great Recession; the year-over-year price gain in March was an astronomical 13.2 percent, a number that hasn’t been hit since late 2005. The expectation is that April and May figures will push this up even higher.

He argues that this isn’t a bubble:

The previous housing bubble was caused by a surge in demand for mortgages, as loosened underwriting standards and exotic mortgage products gave more people the opportunity to buy a home, including many who couldn’t afford it. Today, we have a problem of supply: there just aren’t enough homes for sale. If no other homes were added to the market, the existing stock for sale in March would have dried up in just two months. That’s a record, and it stands to reason that if you don’t have many homes for sale, prices will shift upward as bidding gets intense.

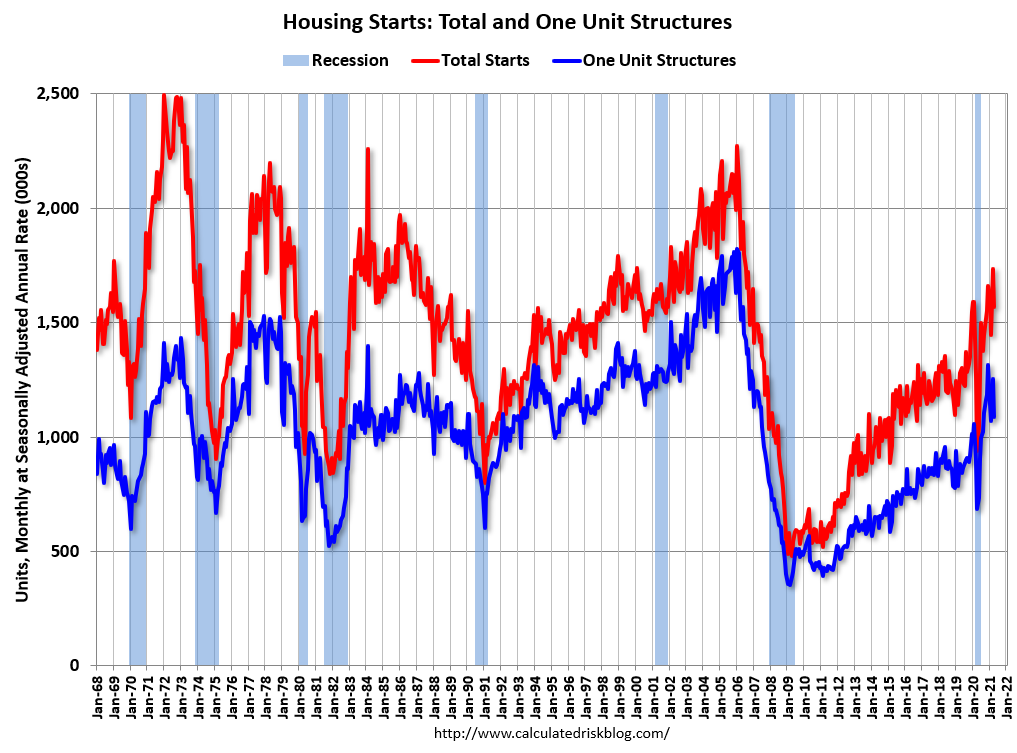

The reasons for the lack of supply may seem like an artifact of pandemic uncertainty, but the causes go back much further. After the housing bubble burst, home builders grew extremely wary of returning to a business that had imploded so spectacularly. For the first two years after the crisis, housing starts remained below any point in the previous 40 years, and even when they rebounded, as late as the beginning of 2020 they remained at a middling level. At the end of 2020, Freddie Mac estimated a shortage of 3.8 million homes nationwide.

The early months of the pandemic further cratered new home construction, and worse, set expectations for sales of components like lumber artificially low. When home buyers did come back seeking mortgages, there just wasn’t enough lumber to physically build the homes. In the last month, unbuilt homes that have been sold but not constructed rose by 16 percent...But this is not quite like the financial crisis, where borrowers could get caught with an unaffordable home payment. Most of the really bad types of loans, like adjustable-rate mortgages that would spike after a teaser period, have been drummed out of the market. “Dodd-Frank really changed the mortgage market; you don’t have terribly underwritten mortgages,” said Arthur Wilmarth, finance expert and professor emeritus at George Washington University Law School. That means that while people are probably overpaying for mortgages, they have been judged to be able to afford the loans...

{kind=link}

We also learned from Black Knight that only 4% of homeowners have a loan for 90% or more the value of their home; 10% equity is “typically [adequate] to sell through traditional real estate channels to avoid default/short sale”. In other words, nothing like the housing bubble of the 2000s when millions of homes had barely any (or negative) equity.

We are still on track to avert a foreclosure armageddon

Black Knight’s most recent data are very encouraging. According to Black Knight’s most recent data, the delinquency rate of US mortgages dropped again, to 4.66% (this number includes loans in forbearance). Overall, 63% of borrowers who entered forbearance are in the clear: nearly half (46%) were able to resume their normal monthly payments, and 17% averted disaster by refinancing (thus obtaining a lower monthly payment) or selling their home (and avoiding foreclosure). Indeed, rising prices made it easier for delinquent homeowners to refinance or sell.

In April alone, 400,000 delinquent borrowers caught up on their mortgage, including 171,000 who were more than 90 days behind. Though the situation continues to improve, 2.18 million borrowers remain in forbearance, including 1.8 million borrowers who have been delinquent for 90 or more days. But as we discussed last issue, there is ample time to avoid a foreclosure armageddon.

We are a nonprofit organization. All of our content is freely available and most (including this newsletter) is reusable under a Creative Commons Attribution License. Our mission is to educate the public about the urgent need for reform of the American housing system and successful housing systems that point out how we can secure housing for all.

Please send in tips—you can do so in the comments or reach us through the web at housing4.us.

We’re interested in any reporting or resources on housing, even if they are several years old. Reporting does not need to have a national scope; local reporting is great!

We especially want to hear if you had a housing-related tragedy happen to you. In our housing system, tragedies happen every day and could happen to anyone. But unless more people understand this, nothing will change. Consider letting us share your story so what happened to you never has to happen again.